Nigel Corea

Senior Program Analyst

Electricity is no longer a background assumption in real estate underwriting; it has become a direct driver of cost, timelines, and asset value. Investors who factor energy into their portfolio strategy today will have the advantage as grid constraints persist and the market continues to adjust. In addition, AI and electrification regulations/initiatives will significantly increase electric use in the near-term, which poses high risk to grid infrastructure that is struggling to keep up.

Grids in the US are under pressure, and the consequences are impacting project timelines, operating budgets, and property values. Investors who don’t pay attention to energy are not underwriting risk of an increasingly important part of their portfolios.

Here’s what’s driving the problem and what investors can do about it.

Why Grids are Struggling

Several trends are affecting electric infrastructure nationwide simultaneously.

- Data Centers and AI

The explosive growth of AI has triggered a massive surge in power demand. Data centers may account for nearly half of all new U.S. electricity demand through 2030. That load is concentrated in specific markets (Northern Virginia, Phoenix, Dallas, Columbus, Chicago) where it competes directly with commercial developers for capacity.

- Electrification

EVs, heating electrification, and electric appliances are all adding load to a system designed for a different era. U.S. electricity demand hit a record and is projected to keep climbing. Many jurisdictions are requiring electrification in commercial buildings as part of a larger effort to decarbonize the local environment, which increases strain on the grid.

- An Aging Grid

Roughly 70% of U.S. transmission lines are over 25 years old, with the majority being 50 to 75 years old. Transformers that once took 12 weeks to order now have lead times exceeding two years. The gap between what the grid can reliably deliver and what customers need is closing, and real estate owners are absorbing the consequences.

The Key Risk Factors Explained

- Rising Utility Rates

Energy costs are climbing fast, and for property owners with significant utility exposure, it’s becoming an NOI problem. The national average commercial electricity rate has risen 37% since 2020. In California, PG&E has projected rate increases approaching 50% through 2027, driven largely by wildfire mitigation investments. Commercial customers in the PJM (the electricity transmission network that supplies the mid-Atlantic) are facing total retail electricity rate increases of 15-30% over the next 24 months. Overall, owners that budgeted 3-5% annual utility increases are absorbing 10-15% (or higher) instead. While an owner’s cost burden depends on lease and billback structure, sustained rate increases can affect tenant economic health and retention, and property NOI.

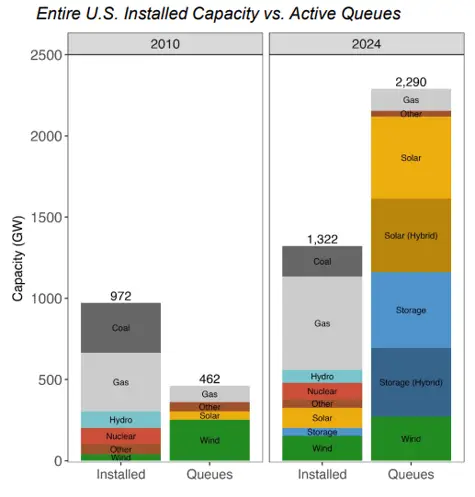

- Grid Capacity

Source

A project approved to break ground in 2026 may not receive full electrical service until 2028 if the local substation is already near capacity. Interconnection queues now represent over 2,000 gigawatts of waiting capacity nationally, more than the country’s entire installed power base. This can significantly delay new development timelines depending on the location substation’s capacity.

- Power Reliability

Climate-related events, such as extreme heat, winter storms, and wildfires, are stressing a system that wasn’t built for current demand levels. In 2021, Texas was subjected to rolling blackouts due to an ice storm that taxed its power grid and left more than 4.8 million customers without power and at least 246 people dead. simultaneously lost power when a single piece of equipment failed on a transmission line. Several grids nationwide are currently or will be subject to rolling blackouts in periods of high demand. This affects existing property values and insurance costs, as areas prone to outages carry higher business-interruption risk, while properties with backup power or on-site generation increasingly command a premium.

- Data Center Pressure

Data center concentration drives up local electricity prices and delays interconnection for all users. At the same time, markets with available power and proximity to digital hubs are attracting premium tenants and land values. PJM is encouraging utilities to push the cost of additional capacity back to the data centers as opposed to spreading rate increases over the whole customer base. While there is some recent success with easing the cost burden of data centers, property owners and tenants are already feeling the impact nationwide on their electric bills.

Regional Dynamics

Not all energy markets face the same risk profile. The table below rates each major grid region across the four key risk factors: utility rate trajectory, grid capacity, stability and resilience, and data center pressure.

RTO / ISO Grid Risk Matrix: